Best house markets in us

10 Best Real Estate Markets In 2022

5. Charlotte, North Carolina

- Median listing price: $385,000

- Time on market: 35

Charlotte continues to be one of the top places to live in North Carolina with access to mountains and beaches alike. The cost of living in Charlotte is 5% lower than the national average leaving room for outdoor lovers to experience this beautiful state in all its glory. Charlotte is also experiencing job growth with a 45.2% increase expected over the next 10 years. Top companies headquartered in Charlotte includes Bank of America, Wells Fargo, Amazon, LendingTree and more.

6. San Antonio, Texas

- Median listing price: $285,000

- Time on market: 55 days

San Antonio is currently a buyer’s market, so if you’re looking to become a homeowner in one of the best places to live in Texas, now is the time. This city also offers plenty of fun activities and history to enjoy. San Antonio is rich in Spanish and Old West heritage as it is most famously known as the home of the Alamo. With over 300 days of sunshine per year, residents can expect consistent great weather.

According to a new report from the U.S. Census Bureau, San Antonio is the nation’s eighth fastest-growing metro. The state is also experiencing an increase in six-figure jobs in the San Antonio – New Braunfels metro region.

7. Phoenix, Arizona

- Median listing price: $459,000

- Time on market: 35 days

- Home value increase (over pre-pandemic levels): 30%

Phoenix home values have increased an astonishing amount over the last year – close to 30%. This increase is largely due to demand from a sudden influx of home buyers: remote workers and retirees who want more space for the money. While home prices are slightly above the national average, data from Payscale shows the cost of living in Phoenix is 5% below average, meaning your dollars will go further.

A six-figure home price jump is enough to put Phoenix on the list of “hottest” real estate markets, but the largest town in Arizona has a lot to offer residents. With increasing tech jobs (Amazon, Uber, Shutterfly and Yelp have offices in Phoenix), over 200 golf courses, along with restaurants and nightlife, it’s easy to see why many move to Phoenix.

8. Jacksonville, Florida

- Median listing price: $289,900

- Time on market: 42 days

- Home value increase (over pre-pandemic levels): 5%

Jacksonville, Florida may not ring any bells when you think of a “major metro area,” but Jacksonville is actually one of the fastest-growing economic areas in the country, with over one million residents in the metro area. Jacksonville’s growth is attributed to its strong job growth, as employment opportunities continue to steadily increase month over month.

Jacksonville is also incredibly affordable with the current Jacksonville cost of living at 5% below the national average, and the median list price of properties well below national averages. In this area, the average price per square foot on a three-bedroom, two-bath single family home is a comfy $182 per square foot.

In this area, the average price per square foot on a three-bedroom, two-bath single family home is a comfy $182 per square foot.

9. Atlanta, Georgia

- Median listing price: $400,000

- Time on market: 41

As the economic and cultural hub of Georgia, Atlanta continues to grow year after year, bringing more and more people to the city. With Atlanta’s cost of living just 1% lower than the national average, residents will have plenty of job opportunities in a variety of sectors (financial, real estate, medical, etc.). Not to mention, several Fortune 500 companies call this city home, including The Coca Cola Company, The Home Depot, Delta Air Lines and more.

10. Orlando, Florida

- Median listing price: $350,000

- Time on market: 39

With the cost of living in Orlando 5% lower than the national average, this city continues to rank as one of the best places to live in Florida. Orlando is also one of the top vacation spots in the U.S. with temperatures rarely falling under 60 degrees. Residents of this city also don’t have to pay personal income tax or sales income tax, which can save people a lot of money year after year.

Orlando is also one of the top vacation spots in the U.S. with temperatures rarely falling under 60 degrees. Residents of this city also don’t have to pay personal income tax or sales income tax, which can save people a lot of money year after year.

While Orlando is known for its amusement parks, finding your own pocket of sunshine isn’t hard to come by with over 100 lakes less than an hour away (not to mention spacious golf courses and shopping centers).

Best real estate markets to buy a home in 2023

Even with rising homeownership costs squeezing out buyers, some real estate markets will remain hot in 2023, mostly due to their relative affordability compared with the rest of the U.S., a new forecast finds.

The top places have something else in common, too: They're all located in the South.

Based on a variety of factors, including home affordability, job growth, migration gains and housing supply, the National Association of Realtors (NAR) analyzed 179 markets to determine which will offer the most value to buyers. The data looks back one year from October 2022 and reflects expected demand from buyers in 2023.

The data looks back one year from October 2022 and reflects expected demand from buyers in 2023.

The median price of homes in some of these markets isn't cheaper than the national median of $398,500. However, these cities scored high on other metrics such as job growth or housing supply.

Here are the 10 best places to buy a home in 2023, according to NAR:

1. Atlanta-Sandy Springs-Marietta, Georgia

Median home price: $371,200

With major tech companies such as Apple, Microsoft and Visa opening Atlanta offices in recent years, the city has a robust job market.

The Atlanta metro area remains relatively affordable compared with other regions in the country. Over 20% of renters can afford to buy a median-priced home in the area, based on a calculation that includes a 10% down payment. The national average is 15.1%.

2. Raleigh, North Carolina

Median home price: $460,500

A fast-growing tech hub with low unemployment, Raleigh has seen home prices increase by almost 30% since 2020. With a median home price near $500,000, it is the most expensive of the top 10 markets for 2023.

With a median home price near $500,000, it is the most expensive of the top 10 markets for 2023.

However, "local home listing prices are coming down from this summer's peak, home inventory has increased 188% in the last 12 months and unemployment in Raleigh is lower than it was pre-pandemic," said Jay Nelson, communications director at the Raleigh Regional Association of Realtors, in a recent interview with The News & Observer.

3. Dallas-Fort Worth-Arlington, Texas

Median home price: $390,100

Dallas-Fort Worth is another emerging tech hub in the U.S., with job growth nearly twice as high as the national average, which was 3.4% for the year looking back from October 2022.

While the supply of homes is less than the national average, inventory increased in 2022, with the number of active listings tripling the national average, according to NAR's data.

4. Fayetteville-Springdale-Rogers, Arkansas-Missouri

Median home price: $328,400

Home to three Fortune 500 companies — Walmart, Tyson Foods and J. B. Hunt Transport Services — this metro area is second among NAR's top 10 rankings in terms of housing affordability.

B. Hunt Transport Services — this metro area is second among NAR's top 10 rankings in terms of housing affordability.

It's a growing market, too, with annual population growth of 2% — well above the national average of 0.01%.

Homes are also cheap, with prices second only to Huntsville, Alabama, among this list. The share of renters that can afford the typical home is nearly double the national average.

5. Greenville-Anderson-Mauldin, South Carolina

Median home price: $335,400

While housing affordability is on par with the national average, job growth in this area is strong, especially for high-paying information technology jobs like computer programming or web development.

There are more houses to choose from, too, as the supply of homes in 2022 was more than twice the national average.

6. Charleston-North Charleston, South Carolina

Median home price: $416,800

Of the top 10 rankings, the Charleston area is second only to Raleigh for the highest median price for homes. It's also below the national average when it comes to affordability.

It's also below the national average when it comes to affordability.

However, this fast-growing market has strong migration gains and job growth that is nearly twice the national average.

7. Huntsville, Alabama

Median home price: $327,500

Alabama's most populous city is the most affordable area for homes amongst this list. Just under 30% of renters can afford a typical home with a 10% down payment, which is almost twice the national average.

Growing job opportunities and low cost of living will continue to attract even more movers in 2023, according to NAR.

8. Jacksonville, Florida

Median home price: $398,000

As with many cities in Florida, Jacksonville became a migration hotspot during the pandemic, with home prices soaring by almost 58% since the beginning of 2020.

Jacksonville's house prices are nearly on par with the median price in the U.S., but it's more affordable than other areas statewide, according to NAR.

The qualifying income to purchase a median-priced home with a 10% down payment is about $98,000. That's less than most large metro areas across the state, including Miami, where the qualifying income with a 10% down payment is $140,000.

Jacksonville also has a strong job market and a good supply of homes compared with the rest of the country.

9. San Antonio-New Braunfels, Texas

Median home price: $342,700

San Antonio became a migration hotspot during the pandemic, especially from California, where home prices and the cost of living tend to be more expensive.

The city has become a destination within the state of Texas, too. Many potential homebuyers have migrated to San Antonio from nearby Austin, largely due to cheaper home prices.

In San Antonio, residents earning $85,000 qualify for a median priced home, including a 10% down payment, much less than $130,000 required in Austin. Job growth is also stronger than the national average.

10. Knoxville, Tennessee

Median home price: $331,100

In 2022, Knoxville's population grew by its largest total since 2007, driven largely by its relative affordability compared with the rest of the country as a whole. A robust job market and supply of homes that rebounded in 2022 is expected to keep this market in high demand in 2023.

While home prices in Knoxville skyrocketed during the pandemic, nearly a quarter of renters can still afford to buy a median-priced home with a 10% down payment, which is about 10% more than the national average.

Sign up now: Get smarter about your money and career with our weekly newsletter

Don't miss: Almost half of the ultra-rich haven't figured out how to pass on their wealth, research finds

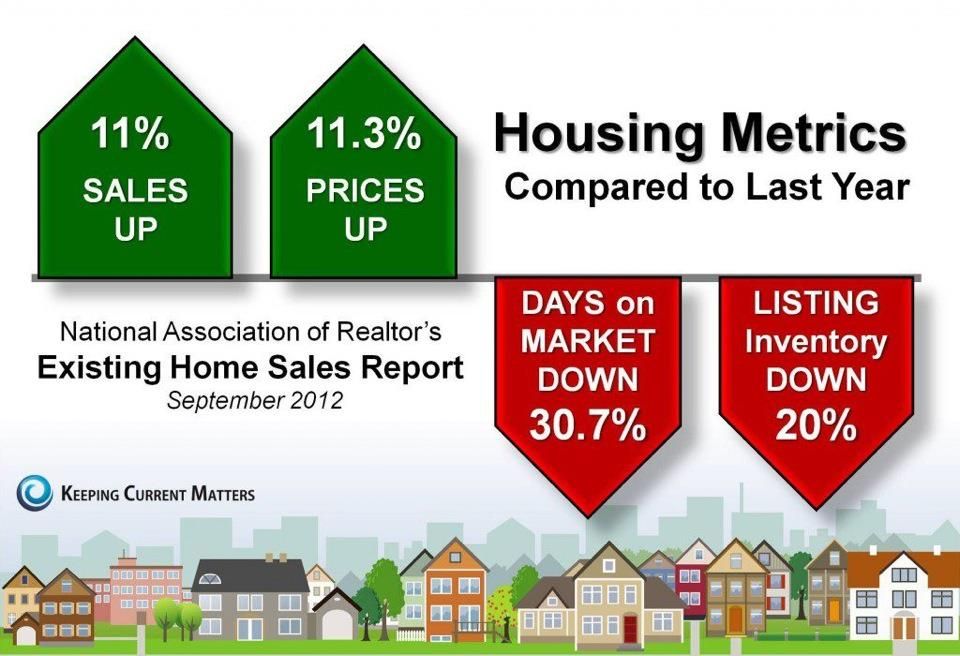

Deals on pause: how mobilization has affected the residential real estate market

Deals in residential and commercial real estate are disrupted or "paused" after the start of partial mobilization. The owners are ready for big discounts in order to speed up the sale and hastily draw up powers of attorney. Banks refuse mortgages to people who could potentially be mobilized, Forbes found out

The owners are ready for big discounts in order to speed up the sale and hastily draw up powers of attorney. Banks refuse mortgages to people who could potentially be mobilized, Forbes found out

The traditional autumn revival in the real estate market, having barely begun, was drowned out by the news about the start of partial mobilization in Russia, said real estate market participants interviewed by Forbes. According to them, the slowdown has affected all segments to one degree or another: sales of residential real estate are in a fever, but rent has dipped slightly. In commercial real estate, the situation is calmer: mainly transactions that are at the initial stage of preparation are postponed for an indefinite period. In the trade sector, experts record individual attempts to break existing contracts.

Forbes polled participants from all segments of the real estate market to find out what has changed in the week since the start of the mobilization.

The suffering elite

The high-budget segment of residential real estate suffered more than others in the first week of mobilization, experts say. Demand noticeably sank here, and deals that were under negotiation were frustrated. “The last week in the sale and rental of high-budget real estate, there was a decline in the interest of buyers. Applications for purchase and lease have decreased by about half both in relation to the previous period and to the same period of last year,” says Dmitry Khalin, member of the AREA board.

“Today, in the premium real estate segment, people take breaks in transactions. This is also due to the expectation of additional price cuts,” says Boris Boriskin, CEO of Skolkovo realty.

“We see a 50% drop in demand in luxury real estate, as it was at the beginning of the pandemic and in February of this year,” complains CEO of Apple Real Estate Danila Savchenko. — Uncertainty about the future is always reflected in the market. Clients who began to return to rent in July-August are now terminating contracts. Some of them go to other regions to be with their families, some go to other countries, and some choose cheaper apartments against the backdrop of the economic situation.”

“The number of calls and visits has halved, several deals have failed, already paid reservations have been canceled,” lists Vera Stefan, commercial director of ASTERUS. “There are those who ask for a delay, some clients have refused transactions, saying that they will buy property abroad due to relocation.” “Last week, two clients at once refused to buy an elite property in Sochi and asked to urgently pick up something for them in Georgia,” says a realtor who works in the high-budget market in Sochi.

Related material

"Center for psychological assistance"

The residential real estate market reacted to the mobilization in different directions: some transactions were stopped, some are being carried out in an accelerated mode, hunters for big discounts have become more active, experts interviewed by Forbes said.

Primary demand (ie property search and calls) is declining. “We record a decrease in potential demand: last week, ads for the purchase of apartments in new buildings were watched 27% less than the average annual values, lots on the secondary market were 17% less frequent,” notes Alexey Popov, head of Cyan.Analytics.

According to him, the rent slipped more modestly - by only 14%. This is confirmed by Oksana Polyakova, deputy director of the department for renting apartments at Inkom-Nedvizhimost. According to her, there are no jumps in the mass rental market, demand, as before, is mainly formed by citizens of neighboring countries.

The perceptions of Forbes interlocutors about the impact of mobilization on the housing market differ markedly depending on the status: large real estate agencies assure that there is no panic and a decrease in demand, while small agencies and realtors working directly with clients talk about minor moods of counterparties.

Large agencies are relatively optimistic. “There were pauses in transactions, but they were short-lived, the peak fell on September 21-22, but after this period the market adapted and most of the transactions were completed. The share of refusals does not exceed last year's figures - 4-5% of the total, and this is normal for the real estate market, ”says Ildar Khusainov, director of the Etazhi company.

“In recent days, we have recorded several cancellations of the reservation - more than usually happens in a week. However, the termination does not carry any landslide-mass character. Panic or excitement in the real estate market is not observed. The participants took a break and are waiting for developments, after all, the real estate market is very inert,” adds Nadezhda Korkka, managing partner of Metrium.

Other experts interviewed report a more worrisome mood. “I have become a social center for psychological assistance… I just tell you how to buy, rent, legalize, open a legal entity, how and where to open a bank account, how to get a residence permit status,” Alexey Shvyrkov Realty, founder of Alexey Shvyrkov Realty, describes the situation. “I would divide my clients into two categories. 20% of those who decided to “try to sell or buy” really put everything on pause. 80% of clients are motivated, they really need to sell or buy a home - and here they are, on the contrary, bit the bit and tried to speed things up, ”says independent realtor Evgeny Konoplev.

Related material

“In the first two hours after the announcement of partial mobilization, we had seven refusals from mortgage transactions at once. People decided to refuse because they are not sure that they will be able to pay the mortgage if their husbands and sons are taken away. Everyone who bought for cash brought their transactions to their logical end, ”says Yulia Usacheva, general director of the Real Estate Agency City Realtor Center (Sochi).

Forbes interlocutors note the willingness of owners to large discounts in order to speed up transactions. “There are a lot of apartments in the residential real estate segment, the owners of which want to sell them within a few days. Obviously, these are those who want to sell and leave the country. They throw off clean apartments, that is, it is impossible to say that these are problematic objects, ”says Valery Letenkov, general director of the Moscow Real Estate Investment Agency.

“In some cases, apartment prices have already been reduced by 5% or even 20%,” says independent realtor Vadim Rumoynikov. “The number of apartment sellers has increased dramatically, applications for the sale of objects are constantly coming. At the same time, sellers are ready to give a serious discount to a “fast” buyer, ”says Kirill Flutkov, an expert on the Sochi real estate market.

“All the potential customers of the last week have asked for significant discounts, as they are confident that the market for HOA will collapse in prices in the near future. I think the market will be completely calm in the coming weeks. People should realize the situation, accept it and draw conclusions,” sums up Maxim Lazovsky, owner of the Dom Lazovsky construction company.

On trust

Real estate market participants talk about a sharp increase in the number of transactions where one of the parties is a proxy. “This has always been considered a sign of an unsafe transaction, but now you have to accept that this is the new reality and get used to working like this,” complains a realtor working in the secondary market in Moscow. “Now people leave powers of attorney for us to sell their homes, they fly away themselves, and then we send them money,” adds real estate expert Georgy Patanin.

A representative of the press service of the Federal Notary Chamber of Russia confirmed to Forbes that the demand for power of attorney has increased significantly over the past week. The interviewed lawyers also note an increase in interest both in the execution of powers of attorney and in consultations on trust management of assets. “Powers of attorney for the disposal of real estate are issued by both individuals, primarily men, and company executives. The situation changes every day, so it will not be superfluous to insure yourself and your business with the possibility of making transactions in someone’s absence,” says Elena Rybalchenko, BGP Litigation advisor.

“We are seeing an increase in the number of requests from citizens regarding inheritance, division of real estate and options for ensuring the protection of rights and legitimate interests in relation to real estate mobilized or subject to mobilization in the event of their possible death, captivity or loss,” says Alexander, partner at the law firm a. t.Legal Pavlovsky. “We also see an increase in the number of requests for paperwork relating to the transfer of real estate for temporary possession, use or management by third parties for the period of mobilization.”

Related material

New buildings on pause

The primary housing market also felt a decline in demand, but, according to interviewed developers, there are no signs of collapse or panic yet. “Some potential buyers of real estate with a mortgage have postponed the decision, taking a wait-and-see attitude. There are also isolated cases of refusal. But in general, the situation remains even at the moment, ”says a representative of Leader Group.

“Some have put deals on pause, as they believe that they or their family members may be subject to mobilization,” adds Sergei Terentiev, Director of the Real Estate Department of the CDS Group. “In such a situation, many people prefer not to take on additional obligations to pay off a mortgage loan, at least until the situation is clarified, because new information comes in every day, and it is quite difficult to understand it.”

“There are clients who have taken a break, and there are those who are in a hurry to close a deal in a short time,” says Anton Vyugin, Commercial Director of MonolitHolding.

Bank refusals

“Demand is being dropped by banks that have begun to refuse mortgages to those they think they can mobilize,” complains a representative of a large Moscow real estate developer. Several Forbes interlocutors at once confirmed that they were faced with the problem of coordinating mortgages for male clients. “Yes, there are mortgage denials for people who fall under the mobilization,” says real estate expert Georgy Patanin.

“Banks have changed the algorithms for assessing the borrower, and there are already cases of refusals on previously approved transactions,” says Stefan from ASTERUS.

Forbes interlocutors did not name specific banks in which they faced refusals. A representative of one of the major banks confirmed that when approving a mortgage, "mobilization risks are taken into account." “All banks are reinsured, because now it is generally unclear who and when they can call,” the mortgage broker specified.

Top 9 Real Estate Markets0001

Europe in matters of business transparency, of course, is in many ways an example for other countries, but the Old World also has its own peculiarities and problems.

Despite the fact that in most countries transactions are carried out quickly and safely, government actions in the tax and legislative spheres are predictable, and regulators fully disclose financial information, Europe is far from homogeneous.

Based on a study by Jones Lang LaSalle, a transparency rating of real estate markets in European countries was compiled. According to experts, the UK, France, the Netherlands, Ireland and Finland became the leaders of the rating in Europe.

At the same time, the markets of central and eastern Europe suffer from a number of problems that can deter even the most sophisticated investors.

Slovenia, Serbia, Bulgaria, as well as the Russian regions, Ukraine and Belarus, quite predictably ended up at the bottom of the list. At the same time, if in Western Europe the crisis seriously increased the transparency of financial transactions and the real estate market, then no conclusions were drawn in the south and east of the continent.

Ultra Clear

Experts classified nine countries of the world as the highest caste of "extremely transparent" markets, five of which are located in Europe: Great Britain (1), France (5), the Netherlands (7), Ireland (8) and Finland (9).

This category includes the real estate markets of those countries where the legal framework and state control is at such a level that any operation is actually "open". It is extremely easy for both clients and sellers to work under these conditions, since all the steps are prescribed, there are practically no “pitfalls” and “gray clauses of the contract”.

Fairly transparent

Experts categorized most European countries as "rather transparent" real estate markets, where the quality is close to the leaders, however, at the moment, they need time to consolidate the results achieved.

These markets include Sweden with Norway, Spain with Portugal, Germany with Poland, Austria with Hungary and Italy with Switzerland.

Experts note that Europe as a whole remains the focus of free transparent markets, where investment flows from all over the world flow.

The most demanded, as before, are London, Paris and large German cities: the transparency of the local markets attracts real estate investors.

The Fifth Republic has achieved high performance largely due to the implementation of an open data policy, that is, due to the comprehensive disclosure of information about the activities of governments at the center and in the field.

Ireland has gone from “quite transparent” to “extremely transparent” this year, thanks to a real estate boom, as well as the success of the “bad bank” NAMA with debt real estate.

"Translucent"

Problems begin to arise when moving east. The third tier includes Slovakia, Romania, Greece, Turkey, Croatia, as well as Moscow and St. Petersburg.

Romania has taken a big step towards market transparency and entered the top five in terms of improving its position in the ranking. The country is more actively bringing its legislation in line with the requirements of the European Union, and also shows some progress in the fight against corruption and in improving the efficiency of the judicial system.

Turkey, which used to improve its performance from year to year, in the current rating was able to add literally a fraction of a percent. Buying a property in Istanbul is still viewed as a significant investment, but the Turkish market as a whole is not becoming more transparent due to the recent political battles in this country.

Buying a property in Istanbul is still viewed as a significant investment, but the Turkish market as a whole is not becoming more transparent due to the recent political battles in this country.

Opaque and Belarus

Slovenia, Serbia, Bulgaria, as well as Russian regions and Ukraine fell into the lowest caste for Europe. Separately, experts singled out Belarus as the only European country that, according to indicators, falls into the category of “non-transparent”, such as Pakistan and Angola.

There is also movement here. For example, Serbia has significantly improved its performance in recent years, while Bulgaria, on the contrary. Serbia's attractiveness is ensured by the start of EU accession negotiations in January 2014, which will entail changes in legislation.

Experts cite such data on the basis of the Global Real Estate Transparency Index, which is calculated every two years for 102 real estate markets. It is the markets, since the BRICS countries are divided into several geographical segments in the ranking.